{kind=link}

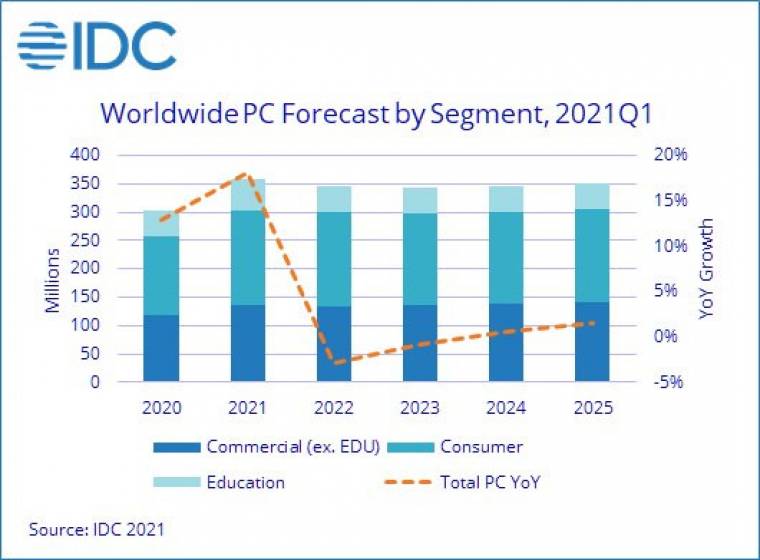

Despite ongoing concerns about the semiconductor shortage, the PC market remains one of the thriving consumer technology markets. IDC Worldwide’s new Quarterly Personal Computing Device Tracker forecasts that PC shipments are expected to grow by 18.1 percent in 2021, with shipments of just over 357 million units. Although IDC still expects PC growth to decline slightly in 2022 (-2.9 per cent), the five-year compound annual growth rate (CAGR) remains positive overall at 3 per cent

” We still get a lot of questions about the growing semiconductor shortage and its impact on PCs, but it’s important to look at every layer of the problem because a lot is happening throughout the PC supply chain, ”said Ryan Reith, vice president of IDC Worldwide Mobile Device Trackers . “We don’t dispute that the entire semiconductor market is currently tight, but for the entire PC market, it’s a completely different story than in the years before the pandemic. Before 2020, the market was characterized by a CPU shortage and, to a lesser extent, memory and panel shortages. priced components such as notebook panel ICs, audio codecs, sensors and power management ICs (PMICs) are the focus. However, without 100 percent of the components, the finished system will not be shipped, so the bottleneck is the bottleneck. ” – said the expert

“There is a common denominator between the missing components (automotive ICs, sensors, PMICs, display drives), namely that the same technology of 40 nm or older “Mature” technologies account for more than 50 percent of the total capacity of the semiconductor industry, and suppliers are only gradually increasing capacity as they focus on the largest segments and invest more in mainstream and c high technology. IDC expects the deficit to ease by the end of the third quarter of this year. A broader upstream balance for the industry is not expected until the first half of 2022, “said Mario Morales, vice president of the semiconductor program.

As things progress, the three main segments of the PC market – consumer, education and From the point of view of IDC, the consumer segment is the most advanced compared to pre-epidemic levels, followed by the education segment and then the public segment.

“As the shortage of parts will continue next year, we expect that the supply of spare parts will continue to be lower than normal and that it will not be the subject of today’s disputes. at least some of the buyers will end up with desktops instead of notebooks, as the urgency of demand is still high enough for any PC. In the longer term, the consumer upgrade cycle is also expected to drag on slightly as the pandemic has overvalued PCs and consumers continue to spend more time and money on PC games and content consumption, ”said Jitesh Ubrani, head of research at IDC Worldwide Mobile Device Trackers.

Hardware, software, tests, curiosities and colorful news from the IT world by clicking here